As mayoral and council candidates roll out their economic priorities, much of the debate focuses on housing and affordability. But an often overlooked factor underlies all these concerns: whether DC residents have the wealth they need to weather shocks, invest in opportunity, and share in the District’s growth.

Wealth gives people the opportunity to thrive. It’s the money people use to pay for unexpected expenses and invest in their futures. It’s emergency and retirement savings, equity from real estate or business investments, and for some, family inheritance.

Any policies focused on economic stability and growth for households must support the continuum of financial health: helping people meet basic needs, be resilient to financial shocks, and access opportunity. And any solutions must contend with the fact that DC and the region have some of the largest racial and ethnic employment, earnings, and wealth gaps in the country. Policy solutions that help families increase their income without considering the importance of wealth will likely help people survive but not thrive.

Failing to support wealth building isn’t just bad for residents, it’s bad for city budgets. Families with as little as $250 to $749 in savings are less likely to be evicted, miss a housing or utility payment, or receive public benefits after a job loss, health issue, or large income drop. These events can cost cities tens to hundreds of millions of dollars, suggesting that any DC elected official has a fiscal interest in improving residents’ financial health.

Against this backdrop, any serious wealth building agenda in DC must grapple with four realities about how residents earn, save, invest, and access opportunity.

1. Building wealth starts with reliable, livable wages and addressing DC’s gender and racial employment gaps.

DC saw the highest unemployment rate in the country in 2025 (5.9 percent), with the Black unemployment rate hitting 9.5 percent. This rate was largely driven by federal workforce reductions and disproportionately affected Black workers. Pay gaps, occupational segregation, and historical and current job discrimination (PDF) can also affect some residents’ ability to earn enough income to save.

The median income for Black households in DC in 2024 (statistically unchanged from 2023) was $60,591, just over one-third of the $168,800 median household income for white, non-Hispanic households (also statistically unchanged from 2023). Because income is the primary input to saving and investing, persistent employment and income gaps make it far harder for many DC residents to build wealth.

Therefore, narrowing wealth gaps across the District requires addressing unequal access to well-paid, stable employment across neighborhoods and racial groups. In the current climate, that means both getting people back to work and continuing to build pathways to higher-earning jobs. DC launched tools intended to connect displaced workers to existing resources, including unemployment insurance and rental assistance, and has a new AI-powered job search platform. Candidates can track engagement with these tools and work with partners to see that they reach residents who need them. They can also track funding cuts to Adult and Family Education grants, which are showing success in connecting DC’s 40,000 residents without a high school diploma to work.

To continue building high-quality pathways, candidates could consider restoring funding for DC’s Early Childhood Educator Pay Equity Fund, which supports educators, who are predominantly women of color, and securing funding beyond fiscal year 2026 for the HealthCare4ChildCare initiative. DC also has direct control over the salaries of its own employees, including DC Public School (DCPS) and charter school teachers. The average DCPS teacher starting salary is $64,640 in DC, which is less than the $72,551 livable salary in DC for a single adult. Additionally, investing in the development of associate’s programs at the University of the District of Columbia that are aligned with labor market demand and lead to higher salaries, like IT and aviation maintenance technology, could strengthen the region’s education-to-workforce pipelines. In-demand sectors should be closely monitored, however, to account for impacts of AI.

2. Emergency savings can help smooth periods of unemployment and economic shocks, but half of DC’s Black families don’t have $2,000 in emergency savings.

Across DC, about 3 in 4 families have $2,000 in emergency savings, money that helps people weather shocks to income like job loss, and shocks to costs, like unexpected car repair. But savings rates vary significantly across the city, both by geography and by race. Eighty-six percent of households in northwest have $2,000 in savings, compared with 45 percent in southeast (here I use public use microdata areas to match Urban’s data dashboard. These do not directly correspond with DC ward boundaries) As a result, many families remain vulnerable to relatively small financial shocks, like an unexpected car bill or increases in utility bills, which can lead to shutoffs and evictions.

In addition to having enough resources to save, residents also need access to savings vehicles themselves. DC already operates a matched savings program, Opportunity Accounts, which is one approach to supporting short-term savings and financial resilience. Expanding access to programs like this to all District employees or others could help strengthen households’ capacity to save for the future. The District could also consider reporting on-time payments to such a program to credit bureaus (PDF) to support credit building among participants.

3. Programs like baby bonds can reduce the racial wealth gap and support educational goals for DC’s youth.

Though median Black wealth has grown in past years, the racial wealth gap remains roughly seven to one. In 2021, DC took a step toward investing in its children with the Child Wealth Building Act, which established publicly funded trust accounts for every child born on Medicaid in the District. Since then, the program has been nullified and the funding cut.

The Urban Institute's modeling on early-life wealth building accounts found that these accounts can increase wealth for all racial and income groups, with the greatest effects for families with the lowest incomes. They also decrease wealth disparities between racial and income groups and the amount of student debt borrowed and the rate at which people borrow. Evidence from child savings accounts in Oklahoma and San Francisco also suggests that automatic, seeded early wealth building accounts can strengthen parents’ commitment to their children’s educational success and increase college enrollment for underrepresented groups (PDF). Together, this research underscores how early-life wealth building can create financial stability for everyone while advancing long-term educational goals in the District.

4. Capital—in the form of a baby bond, down payment assistance, or cash—is not enough to build wealth in cases of poor credit health.

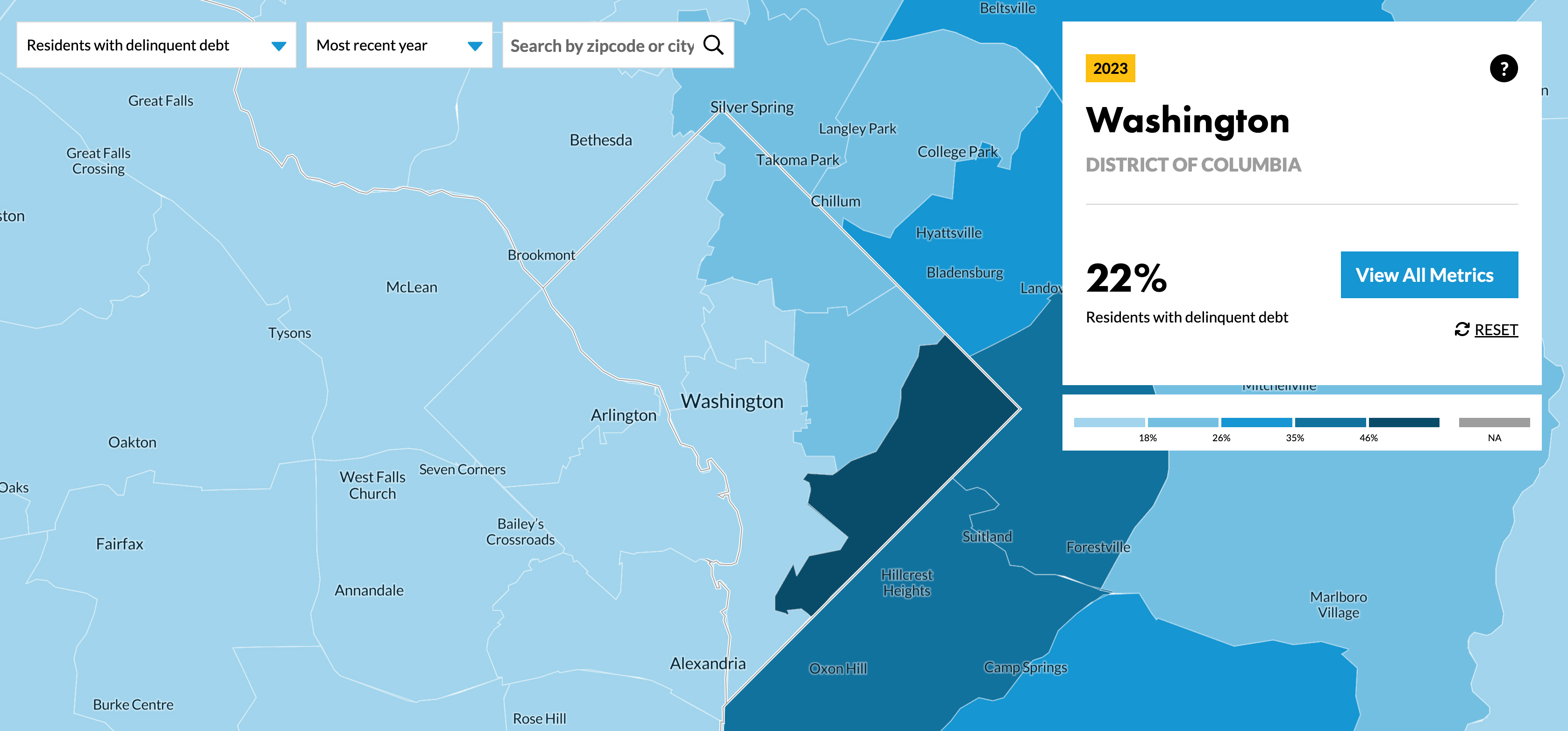

Residents in Southeast DC have the highest rates of delinquent debt (49 percent), more than double the District and national averages (22 and 23 percent). The median credit score in Southeast, at 619, is 100 points less than the District’s median score of 719.

Southeast DC Has the Highest Rate of Delinquent Debt in Washington, DC, 2023

These differences mean that even when resources are available, some households may be unable to convert capital into lasting wealth. Understanding credit health as a structural barrier—not just an individual challenge—is essential for designing policies that expand access to opportunity across the District.

Candidates can consider ways to leverage existing coalitions and resources to provide high-quality credit-building and credit-counseling opportunities starting early in life and continuing throughout financial milestones. For example, for young adults new to financial institutions, such as those in the Summer Youth Employment Program, DC BankOn coalition banks can offer unique products, like the credit-builder loans in MyPath Credit (PDF), which help young adults demonstrate creditworthiness while they’re enrolled in these programs. Financial education delivered alongside any workforce program can also include up-to-date credit information. The Office of Financial Empowerment could also consider a rent-reporting pilot, similar to Rochester, New York’s, which captures on-time payments and helps residents establish or improve their credit.

Wealth building should be a top priority

As DC’s next mayor and council confront a tight fiscal environment and growing affordability pressures, wealth building needs to be at the forefront of agendas. It shapes families’ resilience and public budgets alike.

Let’s help communities build more secure, hopeful futures.

Today’s complex challenges demand smarter solutions. Urban brings decades of expertise to understanding the forces shaping people’s lives and the systems that support them. With rigorous analysis and hands-on guidance, we help leaders across the country design, test, and scale solutions that build pathways for greater opportunity.

Your support makes this possible.